BiQ: CorMedix Q4 Earnings (CRMD)

Investing would be a lot easier if changes in the share price were accurately correlated with a company's future outlook. One could simply buy shares as the price rises and sell as the price declines. Although this is sometimes true in practice, I find that changes in a company's share price are, more often than not, unreliable indicators of the future, especially when it comes to investing in small-cap biotech companies. The hard part is determining whether a sudden decline in the share price is an opportunity—or a warning.

CorMedix (CRMD) released Q4 earnings today. Since top-line numbers had been pre-announced earlier in the year, there were no real surprises in the Q4 or 2024 FY numbers. The company demonstrated impressive revenue growth in the first year of the launch of DefenCath and achieved profitability within four quarters, a noteworthy achievement. However, despite the solid progress in Q4, shares sold off during the day, finally closing at $7.41.

What we will try to determine in the paragraphs below is whether this sell-off represents an opportunity or a warning.

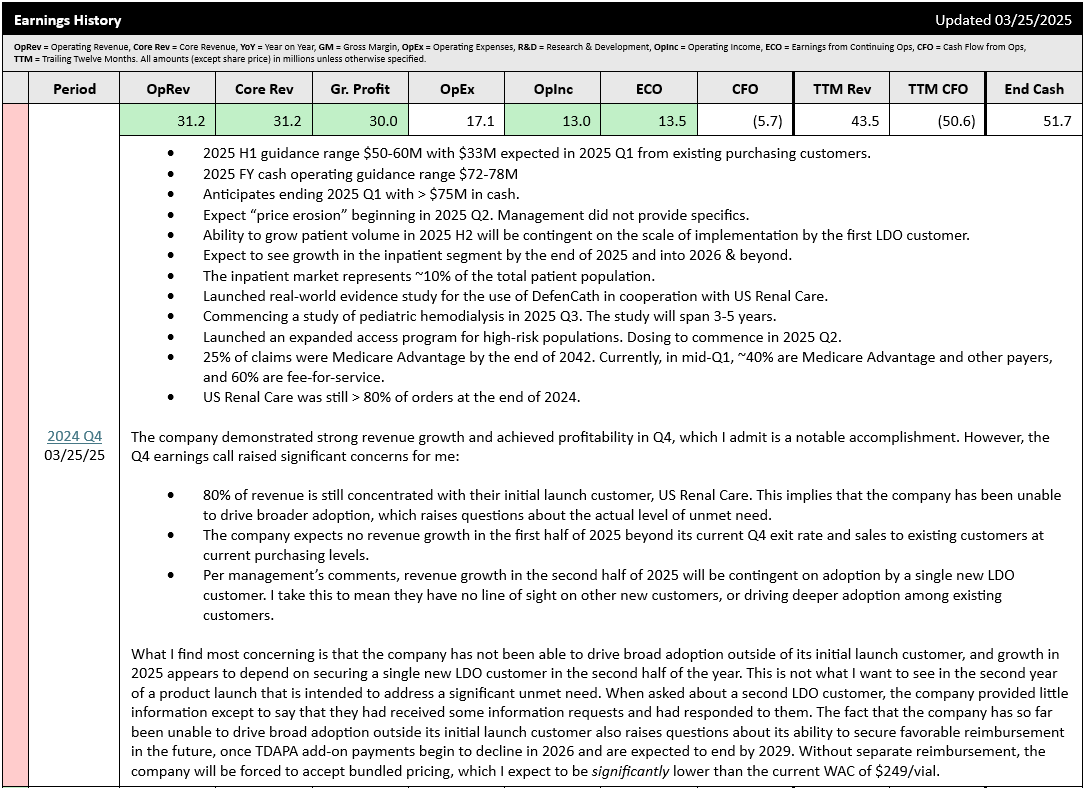

Here is the Earnings Summary I prepared for Q4, taken from the iQ Cheat Sheet:

As I mentioned above, despite the solid progress in Q4, shares sold off by 30% during the day. The bad news, unfortunately, came during management's guidance discussion for 2025. Here is a summary of the key relevant points that stood out to me:

- The company anticipates $50-60M in revenue during 2025 H1 based on purchasing levels of current customers. This represents flat-to-declining revenue in the first half of 2025 compared to the 2024 Q4 exit rate of ~$30M. Although this might appear favorable if viewed through the lens of a year-on-year comparison vs. the same quarters in 2024, I see this as a red flag. I interpret this to mean the company expects flat to negative growth in the first half of 2025.

- The company does not anticipate any significant gains in new customers during the first half of the year and does not anticipate any meaningful increase in adoption by existing customers.

- 80% of revenue is still concentrated with the company's single launch customer, US Renal Care, implying the company has not been able to drive broader adoption at any meaningful level during the first year of launch. This is very concerning to me and raises doubts about whether DefenCath truly fills an important unmet need.

- Revenue growth in the second half of 2025 is contingent on adoption by a single, new LDO (large dialysis operator) customer. When asked about a second LDO customer, management offered very little encouraging information, saying only that they had received some information requests and had responded to them.

Bulls might point out that there are several tailwinds for future growth, including:

- Expansion into the inpatient setting through the new partnership with Syneos Health.

- Expansion into VA hospitals through the new partnership with WSI.

- Adoption by the LDO customer, expected in the second half of the year.

These are all good points and could very well drive greater adoption going forward. However, nobody can tell the future. That's not what investing is about. Investing is about risk and reward. The reward is the fun part, but risk is perhaps the more important part. So, what are the risks going forward?

I already laid out my key concerns above. To summarize, the company has been unable to drive significant adoption outside its launch customer; it is expecting flat growth in the first half of 2025; and any growth in the second half is contingent upon a single new large customer. I see these as significant risks.

Zooming out and looking at the bigger picture, and aside the execution risks I've already outlined, I'm no longer convinced that DefenCath fills an important unmet need. Having 80% of revenue still come from the original launch customer is very concerning, especially since the company appears to have no line of sight on any new customers besides the one LDO they've identified. This is not what I want to see for a product that is supposed to fill an important unmet need.

The inability to drive broader adoption also raises another key concern, namely reimbursement. Currently, the company is reimbursed through a TDAPA add-on payment based on a WAC of $249/vial. The purpose of TDAPA is to encourage broader adoption of new products. However, in this case, the company has been unsuccessful in leveraging TDAPA reimbursement to incentivize meaningful adoption outside a single customer.

TDAPA reimbursement rates are expected to decline during the second year, which is why the company anticipates experiencing price erosion in 2025. After year 2, TDAPA rates for years 3-5 are recalibrated to 65% of the previous year's expenditures. This means that for each year after 2025, the company will be reimbursed at ~35% less than the prior year. And after 5 years, TDAPA expires, which means there will be no TDAPA reimbursement by 2029. If the company has not secured separate reimbursement status by then, it may be required to include DefenCath in bundled pricing, which I expect would be a fraction of their current $249 WAC, resulting in a significant impact on gross margins. If you want to know how difficult it can be to secure separate reimbursement, ask the folks at Ardelyx about their experience trying to secure separate reimbursement for Xphozah.

Given the company's current lack of success in driving broad adoption, despite full TDAPA reimbursement, I have significant concerns about its ability to drive adoption in the future or secure separate reimbursement by 2029. Also, from 2026 onward, the company must grow revenue by at least ~35% simply to compensate for the erosion of TDAPA reimbursement.

I can't guarantee what happens in the future. All I can do is examine the current information available and use it to try to identify future risks and potential rewards. In my view, the risks have increased significantly, and the potential rewards have become less certain based on the information presented during the Q4 earnings call. For this reason, I closed my position in CorMedix earlier today at a price of $8.90 (~162% gain) and moved CorMedix to the Probation List at Biotech iQ Premium. I have also downgraded my NMT and LT ratings to a HOLD, and downgraded my NMT and LT outlooks to Bearish and Cautious, respectively.

In the meantime, I will continue to watch CorMedix from the sidelines for any new information that may indicate a potential inflection point in the thesis.

Premium members can view the updated iQ Cheat Sheet for CorMedix on the Biotech iQ website, or by clicking here.

CRMD share price at the time of publication: $7..41.

Biotech iQ is 100% subscriber supported. If you find this information helpful, please spread the word. You can also follow me on X @ Biotech iQ (_Biotech_iQ).

Biotech iQ is not an investment professional, and nothing on this page or this website should be considered investment advice. Please consult with a licensed investment professional as necessary. Past performance is not indicative of future results.

Member discussion