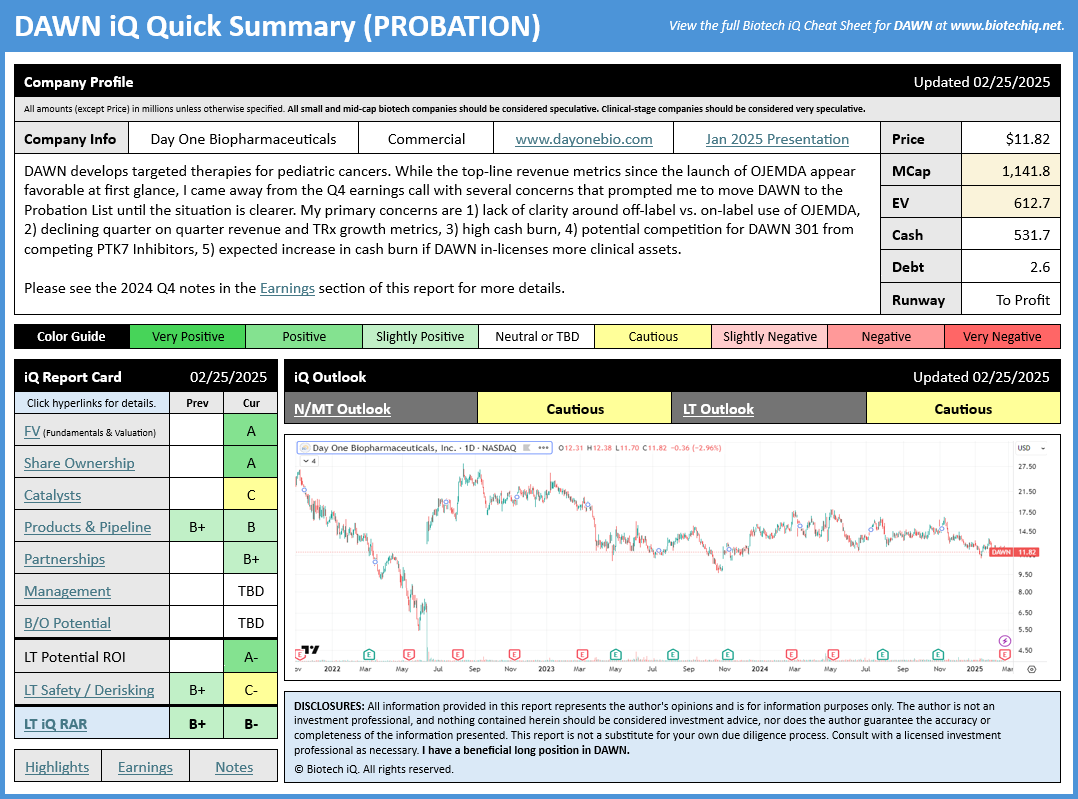

BiQ: Updated iQ Cheat Sheet (DAWN)

After listening to today's earnings call for Day One Biopharmaceuticals (DAWN), I was reminded how important it can be to look deeper than just the top-line numbers to understand the context. While 45% sequential top-line revenue growth looked positive initially, the earnings call raised several concerns for me.

I would summarize my main concerns as follows:

- Management stated that the mDOR of off-label use of OJEMDA is around 4-5 months vs. an expected 24 months for on-label use. While off-label use may be a positive in some situations, in this case, I think it's a negative as these patients will be going off therapy soon. Off-label use can be a bonus, but what matters is on-label market penetration.

- TRx growth slowed in Q4 vs. Q3, and also slowed in Q3 vs. Q2. In Q3, 230 new TRx were added. In Q4, only 181 new TRx were added. Although some allowances can be made for the Holidays during Q4, I would have preferred to see stronger TRx growth this soon after launch. TRx growth rate has been declining each quarter since launch. This decline in TRx growth raises questions about how eager physicians are to use OJEMDA.

- Management stated they plan to use DAWN's strong financial position to engage in BD activities to in-license new products. While this could be positive in the long-term, it also significantly increases near-term cash burn and risks. If management believes in OJEMDA, I would typically expect them to establish the franchise onto solid footing before looking for new assets, especially since they already have two early-stage assets in the pipeline.

- Even if we put aside the $20M one-time in-licensing fee paid in Q4, cash burn remains uncomfortably high at nearly $60M, and in-licensing new clinical assets may further increase cash burn unless OJEMDA revenue growth accelerates.

- Management disclosed at least three other PTK7 Inhibitors are in development by potential competitors, which raises questions about how crowded the field may be for the DAWN 301 program. Remember, every company thinks they have the best drug- otherwise, they wouldn't bother developing it. IMO it's far too early to assign any value to these early-stage assets.

A strong Q1 earnings release could allay many of these concerns; however, until more information is available, I think there are enough questions to cast doubt on the bullish thesis. As such, I am downgrading the iQ RAR and S&D scores for DAWN and moving the company to the Probation List until we have more clarity. As a reminder, stocks are transferred to the Probation List when recent evidence contradicts the thesis and puts the status of the thesis into question.

Please see the updated iQ Cheat Sheet for more information.

DAWN share price at time of publication: $11.82.

Biotech iQ is 100% subscriber supported. If you find this information helpful, please spread the word. You can also follow me on X @ Biotech iQ (_Biotech_iQ).

Biotech iQ is not an investment professional, and nothing on this page or this website should be considered investment advice. Please consult with a licensed investment professional as necessary. Past performance is not indicative of future results.

Member discussion