#Free BiQ: Revisiting Milestone Therapeutics (MIST)

Introduction

With the PDUFA target date for Etripamil, known by the trade name CARDAMYST, for treating PSVT on March 27, 2025, I thought this would be a good time to revisit the thesis for Milestone Therapeutics (MIST). Here are some of the past highlights leading up to the PDUFA in March:

- On May 28, 2023, Milestone announced $125M of strategic financing from RTW investments to support the advancement and launch of Etripamil for PSVT, including $75M of royalty-based financing for commercialization expenses upon approval.

- On October 24, 2023, Milestone submitted an NDA to the FDA for Etripamil for PSVT.

- On December 26, 2023, Milestone received a Refusal to File Letter from the FDA. In the RTF, the FDA did not appear to express concerns about the safety or efficacy of Etripamil, but did seek further clarification on the time recorded for adverse events:

Upon preliminary review, the FDA determined that the NDA, submitted in October 2023, was not sufficiently complete to permit substantive review. The FDA requested clarification about the time of data recorded for adverse events in Phase 3 clinical trials; FDA did not express concerns about the nature or severity of adverse events. Milestone will seek clarification and is in the process of planning a meeting with the FDA.

- On March 28, 2024, Milestone resubmitted the NDA for Etripamil and received notification of acceptance on May 26, 2024 and a PDUFA target date of March 27, 2025.

The Quick Thesis

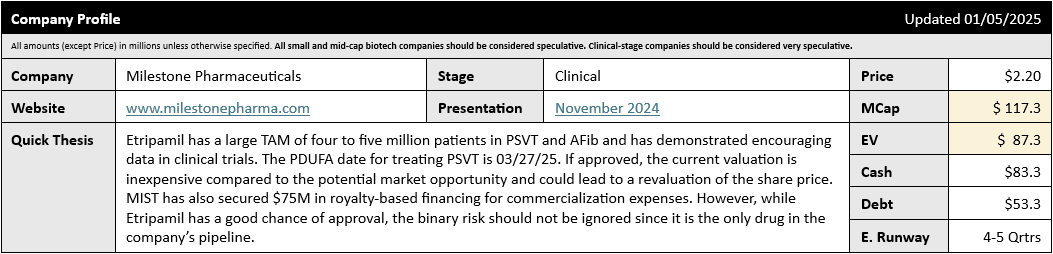

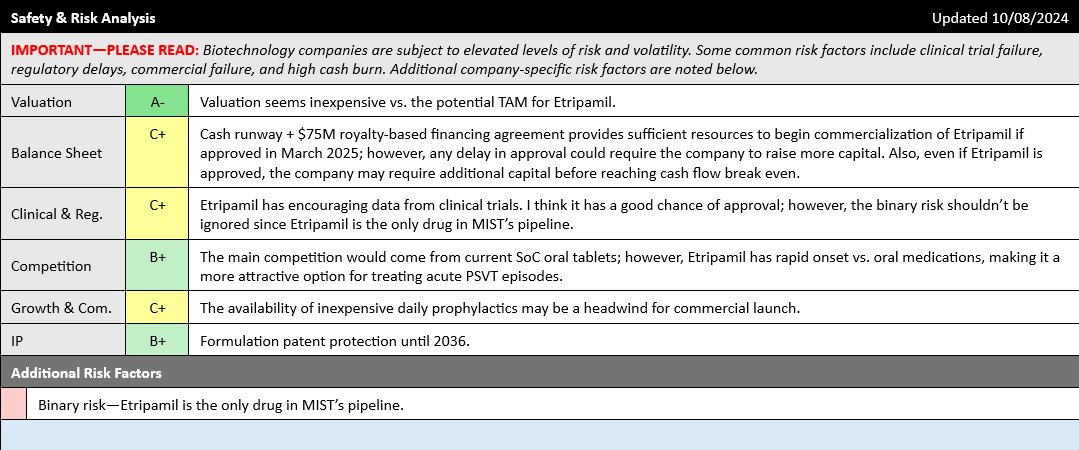

Looking at the Company Profile from the iQ Cheat Sheet, we can see Etripamil has a potential US TAM of four to five million patients across the PSVT and AFib indications. While the PDUFA in March only covers the PSVT indication, the Market Cap still looks very low compared to the potential TAM in PSVT of ~1.5M patients in the US. The company has also signed a licensing agreement with Chinese partner Xi Jin Pharmaceuticals to develop and commercialize Etripamil in China. Licensing options for the ROW remain open.

An approval could lead to significant share price appreciation given the current low valuation; however, since Etripamil is the only drug in Milestone's pipeline, investors should also consider the binary risk should Etripamil fail to secure approval.

The Long Version

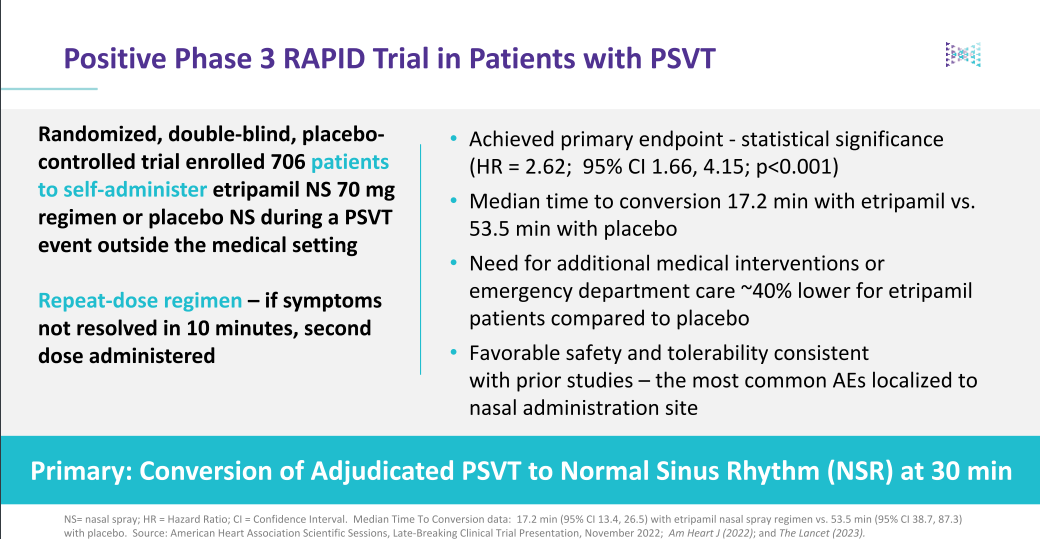

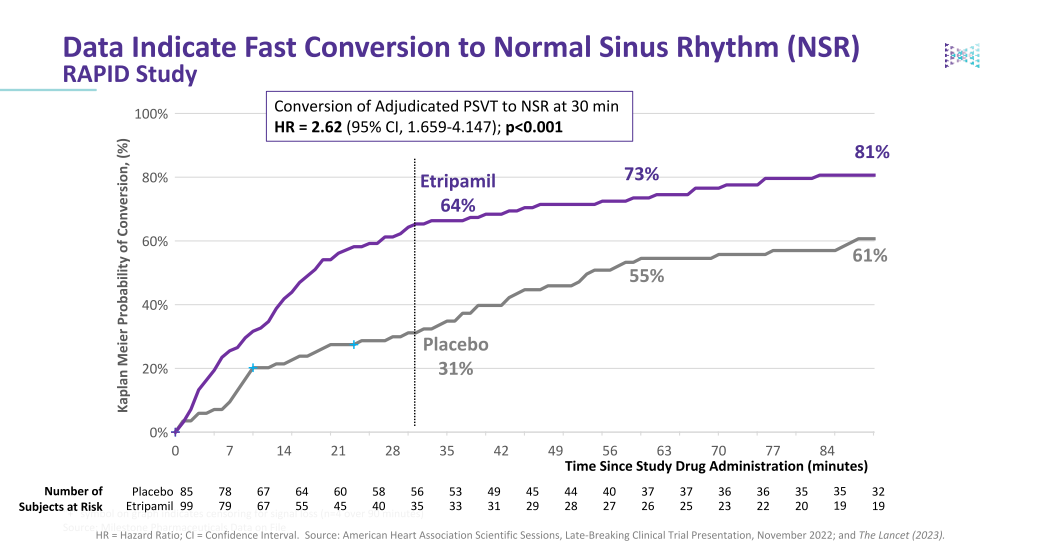

Etripmail is the only self-administered episodic therapy for PSVT that demonstrates a rapid onset of action and fast conversion to normal sinus rhythm (NSR). While oral medications are available, often referred to as a "Pill-in-Pocket", they can take up to two hours to reach Tmax vs. approximately 7-8 minutes to Tmax for Etripamil. This translates to a median time to return to normal sinus rhythm of ~17 minutes for Etripamil vs. ~53 minutes for placebo. Etripamil was generally well-tolerated, with nasal discomfort and congestion being the most common AEs.

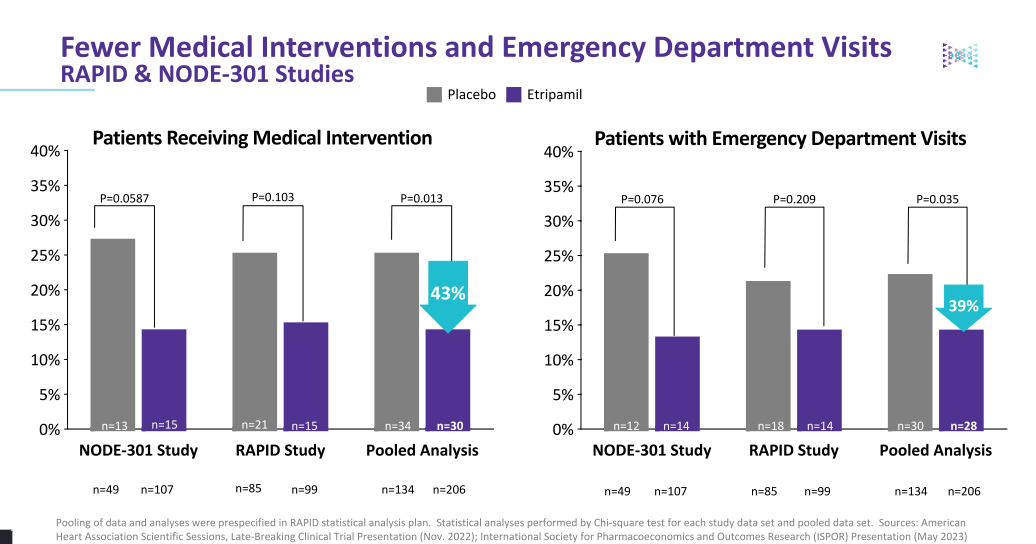

Many patients currently experience one to two PSVT events annually, which often necessitate a trip to the ER for treatment. In a pooled analysis, Etripmail resulted in a 43% reduction in patients receiving medical intervention and a 39% reduction in patient visits to the emergency room.

Commercial Prospects

If Etripamil is approved, the two big questions with any new therapy option are always: 1) Will prescribers prescribe it? and 2) Will payers cover it? There's no way to be sure until we see initial launch and coverage metrics. However, I think there's a good chance the answer to both questions is "Yes."

Etripamil gives physicians a new self-administered treatment option exhibiting rapid onset and a fast return to normal sinus rhythm--potentially requiring fewer trips to the emergency room. This reduces patient anxiety and improves patient care while lowering costs to payers through fewer ER visits and hospital admissions. Another benefit is a potential reduction in the need for cardiac ablation procedures if patients know they can self-administer a safe and effective treatment for PSVT events at home. That being said, there is always risk with any new drug launch. In the case of Etripamil, the availability of oral prophylactics may be a headwind to the wide adoption of CARDAMYST.

Although the company has not provided any guidance on pricing, we can try to arrive at an estimated peak revenue for the PSVT indication by making a few, hopefully conservative assumptions. For this exercise, I'll use a wholesale average cost (WAC) of $200 per dose. If we assume 25% market penetration at $200 per dose and further assume 3 doses per patient per year, we arrive at an estimated peak revenue of $225M, which compares favorably to the current MC of just over $100M. However, remember that these are only assumptions--we won't know actual pricing or commercial uptake until we have more information.

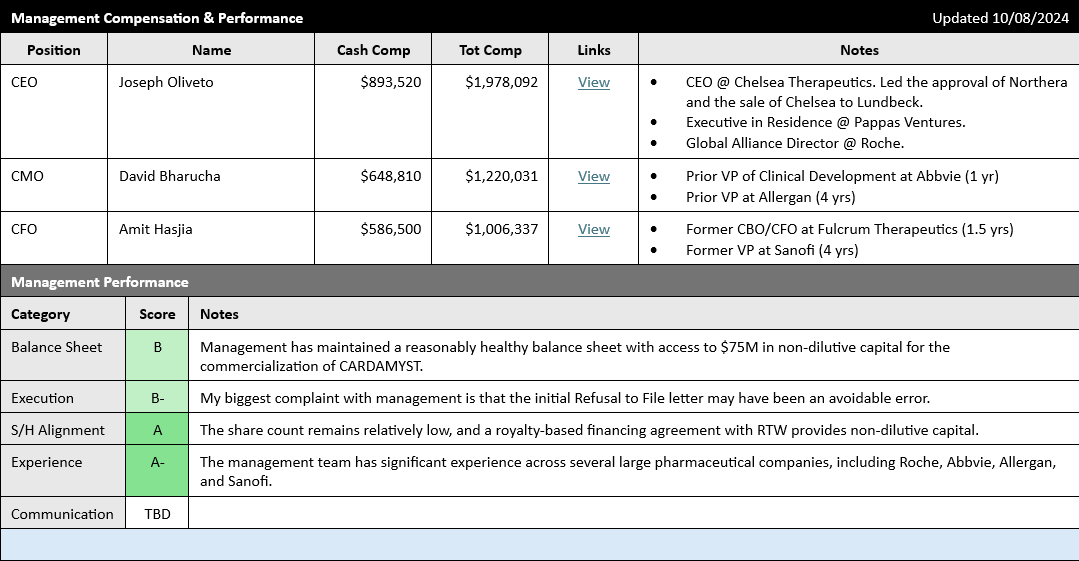

Management

Taking a quick look at the management team, we can see that management compensation seems reasonable, and management has significant relevant experience--including significant experience working at big pharma. While prior big pharma experience isn't any guarantee of success, I still usually see it as a green flag.

Here's a brief description of Dr. Bharucha's prior experience at AbbVie/Allergan:

Dr. Bharucha joined Milestone Pharmaceuticals as Chief Medical Officer in February 2022. He is a cardiac electrophysiologist who brings considerable global drug-development and clinical experience in cardiovascular and multiple other therapeutic areas. Prior to Milestone, Dr. Bharucha served as Vice President, R&D at AbbVie and Allergan where he headed multiple sections including leadership of innovative programs in cardiology, cardiac surgery, arrhythmia, and hypertension.

And here is a paragraph from CEO Joseph Oliveto's bio:

Prior to Milestone Pharmaceuticals, Mr. Oliveto was President, CEO and a Director of Chelsea Therapeutics International, Ltd. (Nasdaq:CHTP) where he led the company through a successful turnaround that included an NDA filing for, and FDA approval of, Northera™, a drug for the treatment of Neurogenic Orthostatic Hypotension, and the subsequent sale of Chelsea to Lundbeck, Inc. Mr. Oliveto joined Chelsea in 2008 following a two-year assignment as an Executive in Residence at Pappas Ventures, a life sciences venture capital firm, where he advised portfolio companies on strategy and governance. Prior to Pappas Ventures, Mr. Oliveto served in a number of progressively senior positions across several operating areas over an 18 year career at Hoffmann-La Roche Inc., including as a Global Alliance Director for Roche’s partnering organization. During his tenure, he played an integral part in the success of multiple NDA approvals, comprehensive launch programs, and licensing transactions.

One caveat, however, is I was disappointed with the Refusal to File letter received by the company last year on their first NDA submission for Etripamil. It's impossible to know the inside details of the situation, but an RTF due to an incomplete data packet seems like it may have been an avoidable error.

The Risks

Looking at the Safety & Risk Analysis section of the iQ Cheat Sheet, we can see that aside from normal risks associated with any new drug launch (slow sales ramp, higher than expected commercialization expenses, delays in securing payer approvals, etc.), the most significant risk factor is the binary risk if Etripmail fails to secure FDA approval. Even a substantial delay in approval, while probably not fatal, would still likely require Milestone to raise additional cash, possibly through dilutive financing.

Potential challenges with commercialization, especially given the wide availability of daily oral prophylactics, should also be considered. These risks are why I assign a Safety & Derisking score of C+ to Milestone Therapeutics, which suggests that investors interested in the story should remain cautious regarding the risks and exercise prudent risk management.

Conclusion

I think the RAR (risk-adjusted return) here is favorable as I believe Etripmail has a good chance of approval by its PDUFA date. If approved, the current valuation looks inexpensive compared to the potential TAM. However, investors interested in the story should remain cognizant of the binary risk and manage their risk carefully through appropriate position sizing.

I assign a Biotech iQ RAR score of B and a Safety & Derisking score of C+, primarily due to the binary risk and uncertainties about the commercial launch. I also assign a Buy rating for both the Near/Mid Term and the Long Term.

Please click here to view the complete iQ Cheat Sheet for Milestone Therapeutics.

I have a beneficial long position in Milestone Therapeutics.

Biotech iQ is 100% subscriber supported. If you find this information helpful, please spread the word. You can also follow me on X @ Biotech iQ (_Biotech_iQ).

Biotech iQ is not an investment professional, and nothing on this page or this website should be considered investment advice. Please consult with a licensed investment professional as necessary.

Member discussion